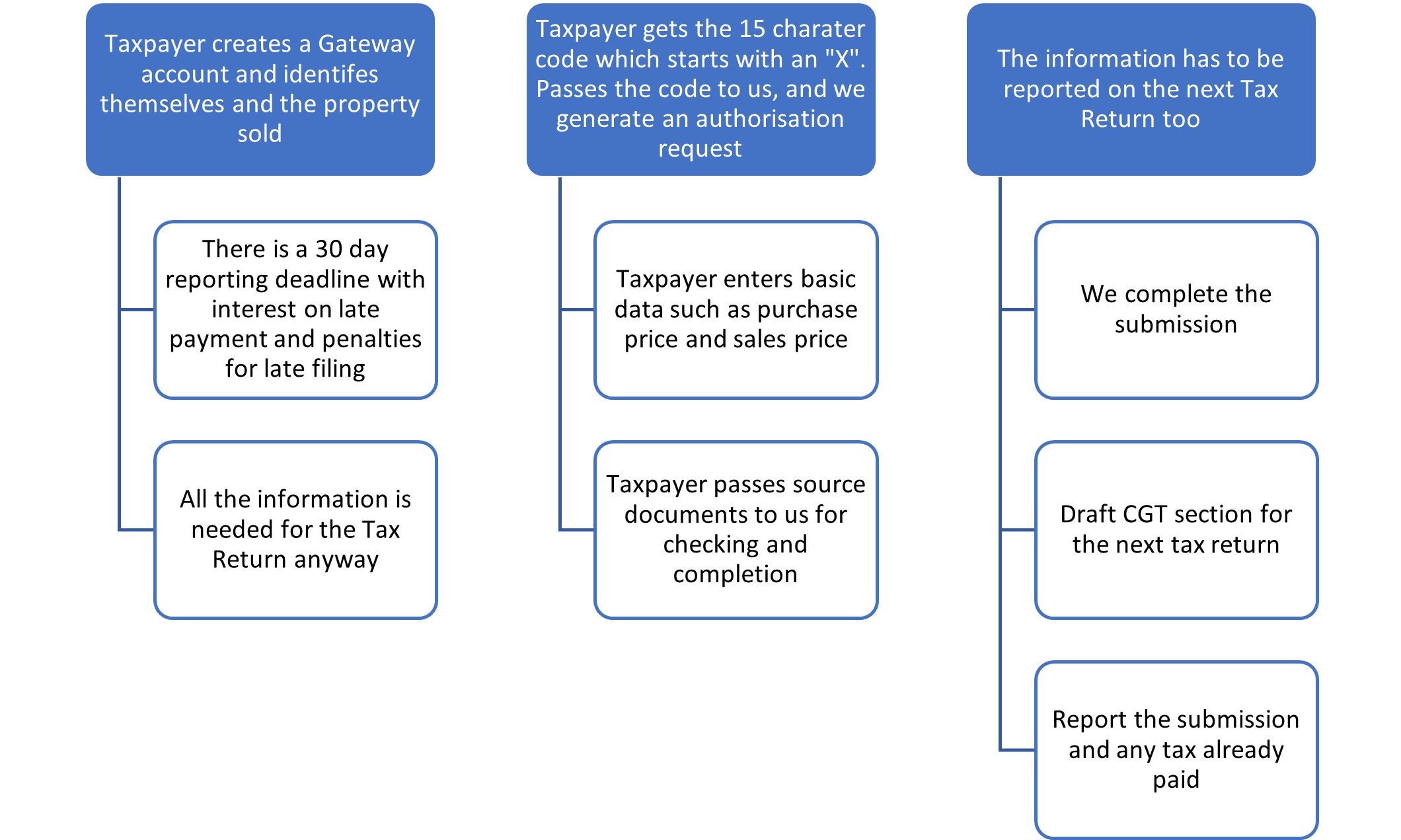

Capital Gains Tax on the disposal of a residential property is required to be reported to HMRC within 60 days of the transaction happening.

This requirement was introduced with effect from April 2020 but it is still not widely known. There are penalties for late filing and for late payment of any tax due.

We would expect the solicitors representing the sellers to advise their clients of the obligation to report, but it appears that this is not happening.

Completing the form is not straight forward except in the most basic circumstances and consequently professional tax advice should be sought. CGT can be quite complex to get right.

How it works

- When you sell the property you must create an online registration with HMRC to report the details of the transaction.

- You register the property address

- Then enter the purchase price and selling price, along with legal costs

- Provide details of any major improvements

- Claim any allowances you may be entitled to

- The portal calculates the tax you are due to pay

- You then approve and submit the Return, and pay the tax due

- Your tax return then repeats the same information along with the submission reference

The reporting only relates to Residential Property. However, the tax return may include other gains or losses for the year. This may affect your overall final Capital Gains Tax liability.

What is a Residential property?

The definition of the disposals caught by the legislation includes any property primarily used as a residence, which is not a hotel or similar. This catches your buy to let property, your holiday home, or a HMO property you own.

Most importantly it catches your main home. If you have lived in the house all the time you owned it then it is almost certain that you will have no tax to pay. But you must still report the gain and claim the tax allowance within 30 days.

It would make sense for you to gather as much information as you can well ahead of the disposal. That makes the process is as painless as possible.

What we can do for you

If we have to submit a Tax Return then you will have to report the gain on the Tax Return too. We will have to enter all that information into our tax software. So we are happy to help you compete and submit the online return. The simple reason is that as we have to do the work anyway It makes sense to get it correct from the outset.

If you get to stage 2 or 3 of the process and provide us with the source documents then we will compete and file the form. We will then update your personal tax return with the relevant CGT information.

How do I get you to complete the CGT report?

When you create the online account you will get a 15 character reference which looks like XJC123CVB456ASD. You can follow this link to sign on to the Government Gateway direct to the relevant page.

Send us this reference so that we can use it request authorisation from HMRC.

We then send the authorisation link to you; you confirm it, and we can proceed.

How much does it cost?

If we are already competing your tax return for the year then the charge will be £50 extra for the online form.

If we do not prepare your tax return, then the charge would be £250 (plus VAT) for the first Return and £50 thereafter.

That’s because most of our work is in setting up the record in the first place. But also we can claim for all the deductions that are available to you.

You will have to verify your identity as part of our Money Laundering processes too.

CGT reporting exemptions

There are a couple of exceptional circumstances where you will have to make a full online submission even though no tax return is due.

You do not need to report a disposal on the tax return where the proceeds are less than £50,000 (2026/27) and your gain is less than £3,000 i.e you have no liability to CGT. Nor do you need to make a report on your Tax Return where no Capital Gains Tax is due. However, if you are registered for self-employment then you need to report all gains regardless.

For more information please contact [email protected]

Due to the complexity and changing nature of U.K. tax law, this advice is only valid at the date of publication. It is not comprehensive and therefore your particular circumstances may not be covered. Taxpayers also need to consider the interaction with other taxes, benefits and their own personal situation. Do not act on this outline without taking professional advice personalised to your individual situation.